From shopping, to ordering food, to notarizations – the global COVID-19 pandemic made electronic transactions a regular and expected part of our lives. For Notaries and their customers, remote notarizations became an option to complete notarizations during the height of the pandemic, when face-to-face interactions sometimes became difficult due to local lockdown measures.

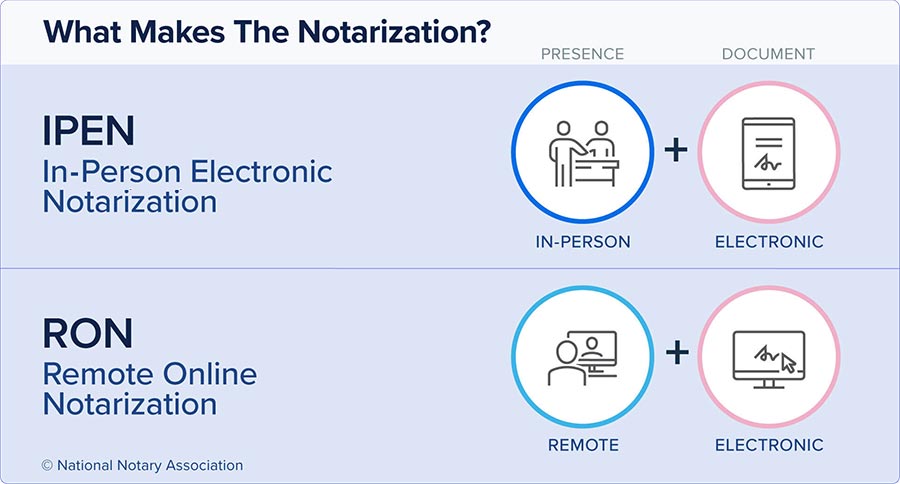

While many states now allow remote online notarizations (RONs) through permanent laws, you may not realize that you were already empowered to perform another form of electronic notarization. In-person electronic notarization (IPEN) has been around for more than 20 years and is approved for use in all 50 states in some form (check your individual state’s laws for the specific requirements for IPENs or other electronic notarizations).

The idea of IPEN was born during the 1990s digital revolution. With the creation of the internet and other digital tools, IPENs were seen as a way to create greater trust in notarial acts. And they were on their way to being widely accepted, but the twin disasters of the bursting real estate bubble and the robo-signing scandal in the mid-2000’s, set back the wide adoption of IPENs. However, with IPEN laws on the books, this type of notarization is just waiting for another chance at adoption.

Remote online notarization demonstrated that there was an appetite for electronic notarizations, but in-person electronic notarization shows how they can be done in a way that is easy and secure — and most of all familiar, because IPENs allow Notaries to follow the same practices and procedures in performing notarizations that they have done for years.

The Notaries I’ve worked with love IPEN for all these reasons, and I expect that the demand will transform Notary businesses, making them more efficient and profitable without sacrificing the trust and security that is expected from the work of professional Notaries.

*(As of September 2022, Alabama, Montana, New Jersey, South Dakota, West Virginia and Wyoming allow remote notarization using paper documents. Illinois, Maine, Vermont, Delaware and the District of Columbia have pending legislation or rules regarding paper document RON that have not taken effect yet. — The Editors)

Brendon Weiss is a Co-Founder of EscrowTab. EscrowTab provides title companies and lenders a software solution to close loans electronically nationwide using its in-person electronic notarization (IPEN) solution.