The increase of digital touchpoints at the start of the homebuying journey is also evident when we explore the evolution of the mortgage application process.

In 2015, Quicken Loans launched Rocket Mortgage, the first completely online mortgage experience. It gave consumers the ability to input their information and get approved for a mortgage completely online. By January 2017, over 25 digital lending firms offered a similar automated mortgage application experience to consumers. Today, the line between digital lenders and traditional banks is blurring.

No longer is there a clear divide separating digital lending newcomers from long-standing lending institutions. In fact, digital front-end touchpoints—especially at application—are nearly ubiquitous among lenders. Our survey found that 92% of homebuyers leveraged online processes when obtaining a mortgage. More than one-third applied for and completed the mortgage application completely online (36%). For returning homebuyers, this percentage jumped to 44%.

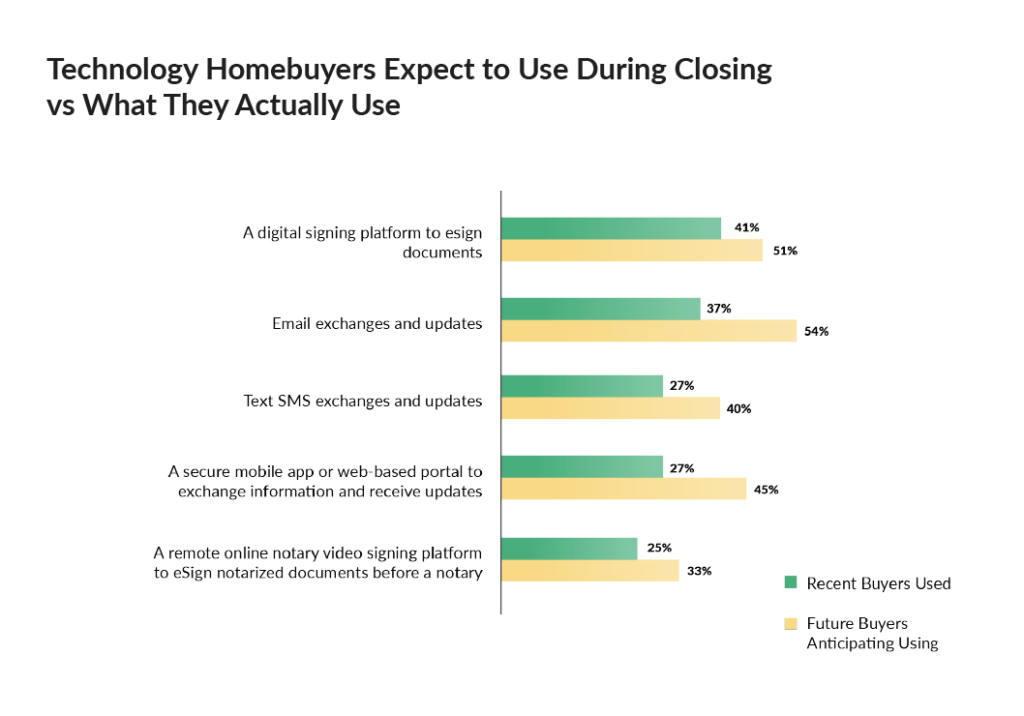

The proliferation of digital tools during the mortgage application process may impact borrowers’ expectations further down the line at closing. Qualia’s survey found that consumers expect a variety of digital touchpoints prior to and during the closing, yet these expectations are largely being unmet.

Overall, there is a sizable gap between the number of technology homebuyers expect during the closing process and what they actually use when they close on a home. The majority (51%) of future homebuyers anticipate they will use a digital signing platform to eSign closing documents; however, only 40% of recent homebuyers report using an eSign platform. Similarly, 45% of future homebuyers expect to use a secure mobile app or web-based portal to exchange information and receive updates, yet only 27% of recent homebuyers report using one.

Over the past year, remote online notarization (RON) eClosings have dominated industry news. And while investment in eClosing platforms has certainly increased for both mortgage lenders and title companies, actual implementation is still lagging due to a number of factors including local legislation, hesitancy among secondary market players, and still-needed coordination (and interoperable technology) between lenders and title companies. Our survey found that only 13% of homebuyers experienced a fully digital closing, yet 62% report that they would like to experience a fully digital closing.